rational market? not for 15 Broad Street loft that sold 13% above unsuccessful 2013 ask

economists weep over the downtown Manhattan loft market (sometimes)

In yet another twist on the Manhattan-lofts-that-sell-above-ask theme, the wrinkle that most interests me about the recent sale of the “2,011 sq ft” Manhattan loft #3120 at 15 Broad Street (Downtown by Starck) that sold $5,000 over ask is that it did not sell when offered at a much lower price last year. With the overall Manhattan residential real estate market up about 10% from November 2013 to September 2014 (according to the single number proxy in the paired-sale StreetEasy Manhattan Condo Index), you’d think that a loft that just sold for $2,605,000 would have sold a year earlier if offered about 10% less than that. You’d be wrong.

Chew on this a bit:

| May 10, 2013 | new to market | $2.295mm |

| Nov 10 | off the market | |

| April 30, 2014 | new to market | $2.6mm |

| Sept 8 | sold | $2,605,000 |

(The inter-firm data-base does not reveal when the loft when into contract, as if there were no REBNY rules about such things; alas.)

Let’s review, if you’ve finished chewing. The loft was professionally exposed to The Market for 6 months last year, without selling. For some reason, the sellers and their agents decided to try again six months later, 13% above the unsuccessful offering. For some reason, they were right.

(Remember: an unsuccessful asking price tells you only that The Market does not like that ask; it doesn’t tell you how far away from The Market that unsuccessful price is. If it were me, I’d guess that the last unsuccessful price was at least 5% too high, on the assumption that someone willing to pay, say $2.18mm, would have been able to successfully negotiate that modest discount last year, with the possibility of a much higher miss. After all, that $2.295mm was the original asking price in that marketing campaign, so you can reasonably assume there was some discount the4 sellers were willing to take.)

what’s not to like about this FiDi loft, apart from the obvious?

There is a significant portion of Manhattan loft buyers who would never consider this 2006 uber-loft conversion because of the oppressive (to some) security measures involved with living across the street from the New York Stock Exchange, even if such buyers would consider elsewhere in the Financial District. But nothing about that has changed since last year, or even since the building was freshly residential.

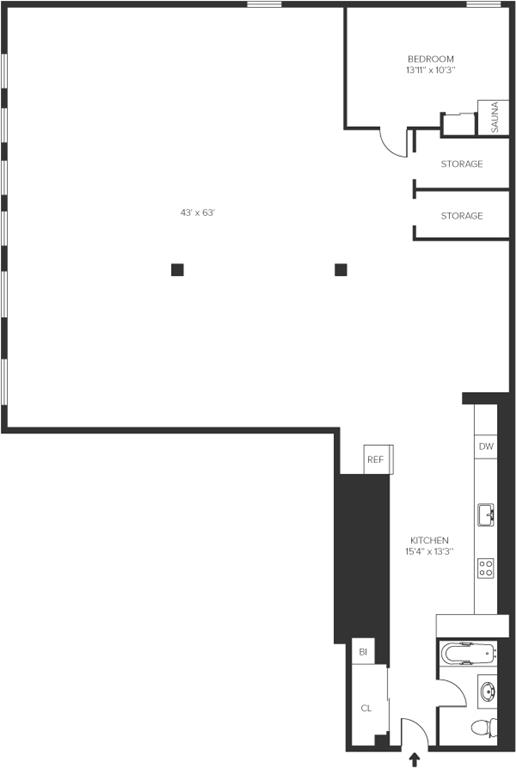

That aside, this loft has many charms: in addition to the standard issue Starck finishes and the super amenity package. Loft #3120 has one of the better 2-bedroom floor plans in the building:

split bedrooms + long walls of windows + corner + large living room

And, from the 31st floor, “breathtaking water and city views from every room”.

Again, nothing about the appeal of this loft in 2014 was not also appealing in 2013, and earlier.

there was an active market at this corner last year

Sometimes there is some hyper-local reason for a loft under-performing The Market, but I can’t imagine what that could be at 15 Broad Street. Among many other sales, two “2,220 sq ft” 3-bedroom lofts on lower floors sold last year just as #3120 was coming off The Market. Loft #1810 sold for $2.85mm in October 2013 and loft #1410 (with the same floor plan and building location, obviously) sold for $2.7mm in November 2013. Neither claimed the views (including the river) that #3120 bragged about, though each has the obvious advantage over #3120 of the third bedroom. Yet they sold at or above $1,216/ft at the same time that #3120 was languishing at $1,141/ft.

Let’s make this even a little worse …. The 3-bedroom market at 15 Broad Street does not seem to have changed much since late last year. The “2,300 sq ft” loft #1620 has a very similar floor plan to the 3-bedroom “10” line neighbors (with no special bragging about views, just about light), and just sold for $2.85mm, or $1,239/ft.

Of course, loft #3120 sold two months ago at $1,295/ft. More, on a dollar-per-foot basis, than the 3-bedroom #1620 last month, after not having sold at least $72/ft lower than #1810 and #1410 last year.

Go figure. I dare ya.

) so that you have a very high level of confidence that you are well advised about The Market. After some months of not finding the loft, you drive a hard bargain for a space that meets nearly all of your criteria, with character, high ceilings, size, in decent (if not mint) condition. It’s been months of looking, involving some dozens of lofts seen in person between $1.5mm and $2.5mm, so you are elated to have found The Right Loft At The Right Price.

) so that you have a very high level of confidence that you are well advised about The Market. After some months of not finding the loft, you drive a hard bargain for a space that meets nearly all of your criteria, with character, high ceilings, size, in decent (if not mint) condition. It’s been months of looking, involving some dozens of lofts seen in person between $1.5mm and $2.5mm, so you are elated to have found The Right Loft At The Right Price.

Follow Us!