Julliard loft at 18 Leonard Street sells up 6% since 2007 (meh!)

sellers got their $500 back

Lofts that sold in the second quarter of 2007 were definitely within the froth that characterized the overall Manhattan residential real estate market leading up to The Peak of sales recorded in the first quarter of 2008. So the recent sellers of the “2,082 sq ft” Manhattan loft #5A at 18 Leonard Street in the Julliard Building were close-to-Peak buyers when they bought on April 10, 2007 at $2,672,500. (In this case, that trailing $500 does not so much indicate a difficult negotiation as it does an effort to differentiate oneself in a bidding war, as the ask was [only] $2.595mm.) Fans of hard bargaining will, however, be pleased by this sequence, in which 2007 buyers became 2012 sellers by driving a hard bargain, and getting their (extra) $500 back … and (seemingly) more!

| Sept 20 | new to market | $2.845mm |

| Oct 3 | $2.875mm | |

| Oct 18 | contract | |

| Dec 19 | sold | $2,832,500 |

That October 3 price bump no doubt signalled to The Market that these sellers were going to be … er … stubborn, which they proved to be as the “$…,500” implies a split-the-difference approach as the last bargaining move.

Let’s do the math. That was a sale late last year at a $160,000 premium to April 2007, a 6% gain over the intervening topsy-turvy 5+ years. If you remember my September 27, 2011, is the Manhattan loft market back to (up to) 2007? 61 repeat sales say “probably”, “a bit”, you remember that this sort of performance was hardly unusual, even as of 15 months ago.

a digression into Market Gain v. Profit

The fact that the market gain from April 2007 to December 2012 (up 6%) says something about The Market, but does not (by itself) imply anything positive for the folks who bought in 2007 and realized this gain by selling in 2012. This is elemental stuff, of course, but let me pedantic and work through these numbers.

From a purely economic perspective, these folks lost money buying and selling. Their buyer brought $2,832,500 to the closing table on December 19, but the sellers had to write some large checks out of that total. Our listing system shows the sales fee was 6%, so the sellers fell immediately into the red when the brokerage firms left with checks totalling $169,950. The red got bloodier when the New York City and State transfer taxes were deducted from this condominium transaction (1.825% = $51,693). The good news, in this direction, is that the buyer is obligated to pay a 1% flip tax as a capital contribution, but that means that in April 2007, these 2012 sellers paid $26,725 into the capital account of the condo, raising their tax basis and increasing their (later) loss by that same amount.

Let’s review. The Market loved this loft 6% more in 2012 than it did in 2007, but that additional love did not help the sellers in the wallet. Having paid $2,672,500 to buy and making the 1% capital contribution in 2007, their initial investment of $2,699,225 overwhelmed their net proceeds from the December 2012 sale: $2,832,500 (minus) 6% sales fee (minus) NYC + NYS transfer fees = $2,610,857, or a personal loss for these sellers (before taking into account other closing costs in either 2007 or 2012) of $88,643.

In other words, the neighbors were happy with an improved comp, but the sellers … not so much.

a(nother) digression about year-end transaction volume

At the risk of delaying further a description of this lovely loft, indulge me with this digression about that meme accounting for high year-end sales volume. (Or, don’t indulge me, and skip down to the next bold sub-head.) I expressed my skepticism about how many late 2012 sales were actually motivated by uncertainty about changes in tax treatment of gains in my January 4, in which Manhattan Loft Guy bravely calls BS on the Market Trend Meme Of The Day, and my subsequent Twitter dialogue with The Miller, and I really do have the intention to more systematically review year-end loft sales (someday! Note to Self …), as I kinda sorta started to do with my January 23, was year-end loft sale at 101 Warren Street motivated by tax uncertainty?.

Even though the loft #5A sale reflects a market gain of $160,000 and even though it closed within two weeks of the year-end, this sale (by itself*) has no apparent tax motivation to close in December instead of January, as there was no taxable gain. One day (after the deed filing back-up gets flushed into public view) I may well look systematically for principled ways to guess which year-end deals fit the meme of Tax Uncertainty Sellers Driving the Market, and which do not. This one will be firmly in the not side of the ledger.

(*Of course it is possible that the sellers really were motivated by Tax Uncertainty to close in December 2012 rather than delaying into January 2013 because this loss would reduce their net gains on other transactions, but starting down that path of considering potential individual tax motivations leads to a rabbit hole of hypothesis upon conjecture based on possibilities. I could imagine some actual Tax Uncertainty Sellers preferring to wait into 2013 to take losses like this, as they would be worth more in a [feared] higher tax environment than a lower tax environment. But that spins that analysis out of control, leading me back to the working hypothesis that there is no principled [data-driven] way to identify Tax Uncertainty Sellers Driving the Market at the scale presumed in the meme, and requiring me to end this digression and return to this lovely loft in Tribeca.)

playing the classic and contemporary card, again (and again)

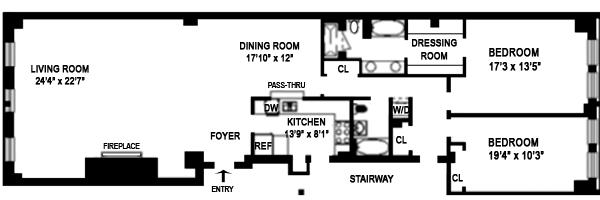

The footprint for loft #5A is classic Long-and-Narrow, with a floor plan featuring two bedrooms splitting the nearly 24 foot rear wall of windows, no side windows, and plumbing on both long walls not quite in the middle. The surviving photos and broker babble from 2007 and 2012 on StreetEasy suggest that the loft itself has not been upgraded in between**, demonstrate the salience of emphasizing fully modern lofts with classic elements, and show how hard it is not to adopt/adapt a prior listing description if you want to hit the same note. Here is the guts of the 2007 babble:

{kind=link}

absolutely stunning 2 bedroom, 2 full bath luxury condo loft is designed to take advantage of the best features of loft-living while incorporating design elements that make the space modern and contemporary. Beautifully appointed, with handsome decorative columns in living room, custom-built mantel gas fireplace and designer lighting fixtures. This exceptional entertaining space is complimented with a Chef’s kitchen that has ample granite counters, cherry cabinets, stainless steel appliances and a gracious-sized dining area adjacent to the kitchen. The master bedroom suite has a large walk-thru dressing area/closet, and a limestone and cherry cabinet master bathroom with Waterworks fixtures, double sinks, a separate stall shower, and Kohler soaking tub. Other features include central A/C and a washer/dryer and high-tech trash disposal system

The 2012 agent didn’t exactly copy, but certainly used the sequence and framework, as well as some phraseology from the other agent’s work (my italics, to note some parallels that jumped out at me):

elegantly designed 2 bedroom, 2 full bath luxury loft is situated on one of the best Tribeca blocks. Its design elements highlight the finest qualities of loft living with very fresh and modern finishes throughout. It is well appointed, with custom-built gun metal gas fireplace with red gum wood mantel, and well designed lighting. The extraordinary flow of the entertaining space is complimented with a Chefs kitchen that has ample granite counters, cherry cabinets, stainless steel appliances and a generous sized dining area adjacent to the kitchen. Both bedrooms have custom built-ins. The master bedroom suite has a large walk-thru dressing area/closet, and a limestone and cherry cabinet with Waterworks fixtures, double sinks, a separate stall shower, and Kohler soaking tub. Other features include an abundance of California closets, central A/C full size washer/dryer and high-tech trash disposal system

My guess is that Agent #2 did not even do this consciously, but I read “mark-up” rather than “compose” in these two bits of babble.

**We have a full set of 2007 listing photos in our system (it was a Corcoran listing), which show that the loft did change a bit after the recent sellers bought in 2012. The huge gun metal element around the fireplace has been added, the kitchen pass-through has been expanded by removing some high cabinetry(most curiously) the two columns referred to in the 2007 babble have been entirely removed (they were on a line just to the left of the entry on the 2012 floor plan; I have never seen that before, though [obviously] they were not structural). The loft looks better without the columns (which had been sheetrocked). Again, I assume they were not structural, and that the upstairs neighbors will stay upstairs.

In other words, with the changes after purchase, the recent sellers’ loss was actually greater than the $88,643 calculated above, the 6% market gain notwithstanding. O. U. C. H.

remember: neighbors love comps that drive values, even if not “profitable”

The neighbors like that #5A sold at a premium to 2007, notwithstanding that the #5A sellers actually lost money. They liked what the #6A owner did a bit more.

I suspect that it is not a coincidence that the neighbor upstairs offered his loft for sale the day after loft #5A went to contract, or that he asked for a tad more than #5A had been asking. (Not because of concern that they took the columns down [d’oh] but because they created an attractive and highly relevant comp.) The other neighbors in this 31-unit condo liked the #6A comp even more than the #5A comp.

Fear not, as I am not going there, except to note that the #6A sale might have had some Tax Uncertainty motivation, as this seller had a gain (he bought in 2004 at $2.1mm), and rushed through The Market:

| Oct 19 | new to market | $2.895mm |

| Nov 15 | contract | |

| Dec 17 | sold | $2.895mm |

The #6A seller either thought that his custom dark wood built-ins looked nicr than those in #5A, or he thought there should be significant premium to being just one flight higher, or he thought that the 5A folks left some money on the table (the “$…,500” notwithstanding). (The babble is similar; I am not going to repeat that exercise.) Net-net, he wasn’t wrong, as he got $62,500 more for #6A in a deal as close to simultaneous as you can get without competing head-to-head. That’s only a 2% premium, but it is real money.

Props to the #6A guy for squeezing that premium out of a buyer who (probably) looked at #5A and passed on that opportunity at an even lower value.

© Sandy Mattingly 2013

Leave a Reply

You must be logged in to post a comment.

Follow Us!