did 30 West 15 Street lofts sell at premium due to combination potential?

numbers are hard things

It is not a coincidence that both lofts on the 3rd floor at 30 West 15 Street closed on the same day. Although owned by different people and listed by different firms, the closings of lofts #3S and #3N were coordinated because they were bought by the same folks, obviously to be combined. One interesting question raised by these sales is whether the buyers paid a premium to get both (following the 1+1=2.5 math VToy in the New York Times explained [but did not well support; see my September 10, deconstructing NY Times article about combining apartments to increase value] and which The Miler takes as a given).

Another interesting question is about the negotiating dynamic, as they signed the contract to buy one before they reached a deal on the other … why give the second seller so much leverage?

Sad to say, these are interesting questions to discuss, but we are not going to get any answers. Numbers being the hard things that they are, it is impossible to prove through comps whether there was a to-be-combined premium. (What data there are suggest the answer is “no”.) And no one is going to reveal their negotiating strategies. But let’s look at the first question, at least, knowing we won’t find definitive answers.

dual histories, curious parallels

The relevant histories for the two lofts begin in 2007:

| #3S | May 3, 2007 | sold | $2,900,000 |

| #3N | sold | $1,737,500 | |

| #3N | June 26, 2008 | new to market | $1,795,000 |

| #3N | Sept 19 | $1,650,000 | |

| #3N | Sept 25 | $1,595,000 | |

| #3N | Feb 11, 2009 | $1,495,000 | |

| #3N | April 22 | off the market | |

| #3S | April 26, 2011 | new to market | $3,100,000 |

| #3N | May 5 | new to market | $1,895,000 |

| #3N | May 31 | contract | |

| #3S | June 21* | contract | |

| #3N | Sept 22 | sold | $1,845,000 |

| #3S | Sept 22 | sold | $3,050,000 |

(*Our data-base has this earlier contract date for #3S.)

The change in value for these two lofts since 2007 for #3S is 5.17%, for #3N is 6.19% … essentially the same. While a nice parallel, this tells us nothing about a Combo Premium. But looking at where these two lofts sit on the spreadsheet of (by now) 71 lofts that sold both in 2007 and 2011 makes it very hard to find a Combo Premium. (See my September 27, is the Manhattan loft market back to (up to) 2007? 61 repeat sales say “probably”, “a bit”, about the overall conclusions to be drawn from those pairs [hint: see hte title] and for how to get free access to the spreadsheet [hint: send an email].)

The short story is that the 2011-over-2007 gains for these two lofts rank 34th and 36th in percent gain among the 48 pairs of lofts that had some gain, then to now. 22 of those lofts showed gains of more than 10%.

You can argue that this method is not an ideal way to measure market changes (the N in the data set is still pretty small), and that one example does not prove anything about The Market, overall. But you cannot argue from this data that the buyers paid a premium to be able to combine these two lofts.

figurative math is not literally math

To be fair to VToy and to The Miller, the argument is not that 1+1=2.5 exactly or in all cases of to-be-combined units. In that September 11 New York Times piece, VToy relies on The Miller for some general points, including that The Combo Premium is more like a “not uncommon” occurrence than a rule, and that it depends on the layout logic of the two units:

Jonathan J. Miller, the president of the appraisal firm Miller Samuel, says the 2.5 in the equation is more figurative than literal. “If you have two adjacent apartments and they logically connect to a bigger and better layout,” he said, “it’s not uncommon to see a 20 percent premium on a price-per-square-foot basis. And that’s before the renovations are even done. It’s just the fact that they’re put together.”

To be sure, not all proposed combinations make sense architecturally, but for two units that can easily be merged, Mr. Miller said, buyers are willing to “pay more for the potential to enhance the value.”

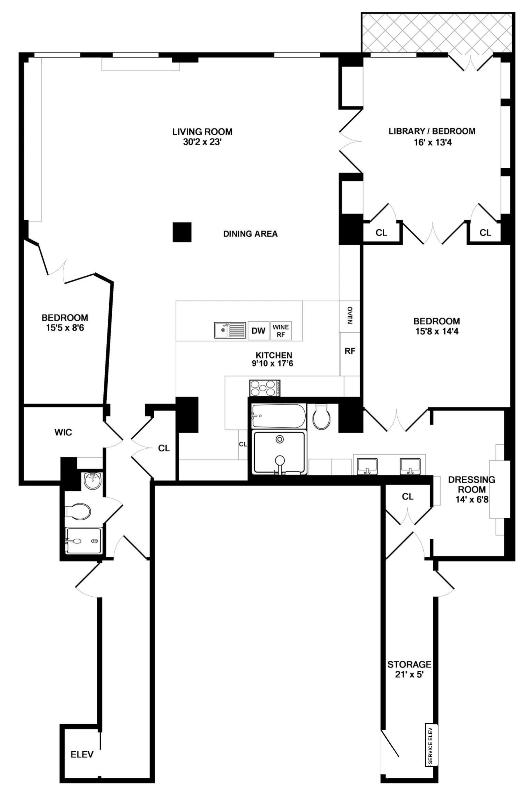

In this case, the proposed floor plan is hardly imaginative, but there are few things easier than combining two lofts that share a wall on which there is plumbing on both sides of that wall (compare the two separate floor plans here for #3N and here for #3S). In fact, the combination solves the biggest floor plan problem in the #3S separate layout: those two long hallways that wrap around part of the adjoining loft are so awkward that one was billed as a 21 x 5 foot storage space. In other words, if you would ever expect to see a combination premium based on both the ease and the logic of the combined floor plan, this pair is that example.

{kind=link}

{kind=link}

{kind=link}

Except that there is no evident premium. At all. Let alone a 20% premium.

a strategy that showed doubt about the theory

These lofts at 30 West 15 Street might not be the ideal test case for the 1+1=2.5 theory because the sellers were not all-in on that theory. Each loft was offered as a stand-alone property, in the case of #3N for almost 4 weeks before contract, while #3S was available to a stand-alone purchaser for 9 weeks before contract. The eventual combo buyer had at least some weeks to see that the individual loft buyers had not (yet) snapped up either loft.

Separate marketing as separate lofts might have depressed the combination premium by making explicit the single-unit market values (lower, in theory). From one of VToy’s sources:

the “ideal way” to market a combination was at a single price. Listing one of the units individually “waters down” the power of the combination… and makes it harder to get as much of a premium, because buyers can see the fair market value of one unit and then “look at the two pieces and argue that they don’t add up to the number you’re asking.”

Perhaps that is what happened here, and that this form of either-or-both marketing is simply not a good test of 1+1=2.5 math. But it should be at least telling (and disappointing for 1+1=2.5 fans) that the professional agents who marketed these two lofts did not persuade the two sets of owners that they could both be as much as 20% better off if they marketed jointly only as a combination, with the theoretical premium baked in to the asking price.

If the theory works, you’d think that the sellers might try that exclusively combo marketing at first, with a back-up plan to split up into separate marketing plans if Plan A did not work. But maybe in the real world getting separate owners (and agents!) on the same page is akin to herding cats.

© Sandy Mattingly 2011

Leave a Reply

You must be logged in to post a comment.

Follow Us!